Odd lots #14; Numbers & Narratives

Did you ever take a decision, where you knew there would be considerable risks, and… you went ahead with it anyway?

1. Intro

Well, long-time stock investors know there’s always big risks lurking around somewhere in the shadows. Personally, having my LatAm cable operator losing 80% of its revenue in Puerto Rico quarter-over-quarter, definitely ranks amongst my biggest surprises or unaccounted risks.

I knew about hurricane risks in the Caribbean, and yet… I definitely did not count on the massive extent of devastation of hurricane Maria on Puerto Rico in 2017.

LCPR revenue development (amounts x 1 million USD)

Luckily, in investing, very differently than with some situations in life, we do not need to put everything at stake when we want to take a chance. Actually, there are some big success stories out there of investors who deploy a deliberate strategy with lots of small positions, in stocks with huge optionality or value creation potential. Potential meaningfully of even big positive impact in the bull-case scenario. Small portfolio loss, when it does not turn out well. I wrote about this strategy when I introduced such a position to Founders, here…

… I would not have had my first 10-bagger (Sintana Energy) — and subsequently my first 10-bagger that shrank into a 3-bagger 😬 — without that strategy. Another stock that I considered to have long-tail upside return potential and high risk, was a ‘roll-up’ story…

A roll-up story where some of the risk materialized, which culminated in the auditor forcing the company to make huge accounting adjustments, whiping out a large portion of the recorded revenues from the previous 21 months, and all-of-a-sudden recording a ton of overhead costs that had been previously capitalized in the inventory position.

Let’s walk through the Numbers & Narrative for that stock with the recent 2025Q1 results…

2. Simply Solventless Concentrates

Ticker: $HASH.v 🏷️

It is awfully tough to rely on reports and accounting after a company was just forced to huge accounting adjustments by its auditor, but… Let’s entertain the thought that the 2024Q4 and 2025Q1 reports are clean now. In that case…

2.a. The Free Cash Flow (FCF) Numbers

… HASH would have CAD 3.2m Free Cash Flow (FCF) burn in 2025Q1.

FCF calculation: 1 + 2 + 3

That CAD 3.2m cash burn figure includes several items that were pretty ‘out of the ordinary’.

Given all the acquisition and business integration activity, I have no problem in believing restructuring & acquisition costs were over CAD 0.4m. Adjusting the cash burn for that amount, brings the underlying cash burn down to CAD 2.8m.

The ‘bargain purchase acquisition price’ gain is also one-off, and can be discarded for this exercise because it did not impact FCF.

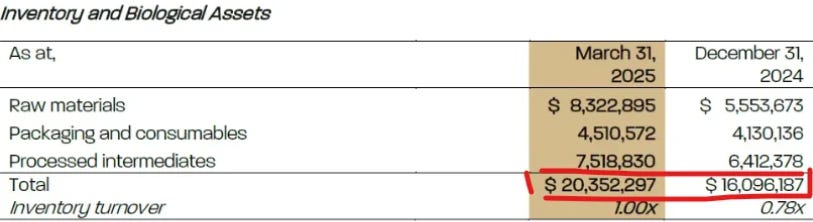

The critical question was and still is how HASH will run its working capital going forward. A further increase in net working capital was once again the factor driving FCF in negative territory in 2025Q1. From 2024/12/31 to 2025/03/31, inventory increased 26% or CAD 4.2m to CAD 20.4m.

CAD 2.664m of that CAD 4.2m inventory build-up was recorded as an organic increase, depressing FCF…

… and the remaining CAD 1.572m was recorded as acquired Cannabis inventory trough the Humble (fka Delta 9 Bio-Tech) acquisition.

What puzzles me is the commentary that “inventory increased 26%… due to the acquisition of Bio-Tech.”

If the full 26% or CAD 4.2m inventory increase was due to the the Humble / Bio-Tech acquisition. Then, that implies that ‘organic’ FCF (HASH without the Humble acquisition) could have been CAD 0.1m negative (CAD -2.8m +/+ CAD 2.66m = CAD -0.1m). That would already be very close to FCF neutral.

2.b. The Narrative

HASH acquired Humble through CCAA proceedings…

Googling CCAA proceedings…

HASH’ acquisitions are frequently purchases of financially-distressed purchases. We can safely say that that was also the case for Humble. And since the deal was a fire sale, it does not sound illogical to me that HASH bought Humble while it was very light on inventory, especially for a new owner with plans to grow that business. That scenario would then require a strong inventory build-up, immediately following completion of the acquisition.

It would also not sound illogical to me, if suppliers to Humble would require advance payments, or at least very short payment terms to supply that inventory. After all, who wants to deliver to a company that was in financial distress?

Rising inventory, without being able to get much supplier credit (= accounts payable) » that was basically the narrative from when I first encountered HASH. This Narrative still does not sound illogical to me, looking at the Numbers.

Cash (generation) was tight at HASH from the start of its (reverse) listing in Canada. That was part of the risk for this particular stock. Overall risks were amplified by the aggressive roll-up strategy. Acquisition after acquisition just makes it extremely difficult - I’d say impossible - to get conviction on the underlying health of the business (excluding those acquired companies) through the reported numbers.

To me the stock looked like a suitable long-tail stock because of the explosive value creation potential from consolidating the industry through acquisitions at distressed asset prices, profitability seemed there, and the company did not have any debt initially. The latter did reduce the risk.

The bears will call out that the company was burning cash, and that it did not have a viable economic model.

Of course it did burn cash! It was buying cash-strapped businesses, and had to invest in building-up working capital. We will find out soon whether the company has a viable economic model, and it can actually generate some cash.

2.c. How further?

For me personally, I am not quite ready to call anything about HASH with a ton of conviction. After all, the accounting change discussion only started to surface in April this year… after, the 2025Q1 quarter-end of 2025/03/31. You can see where my conviction level stood before the accounting issues arose, right here…

HASH reported its shocking audited 2024 results (adjustments) in early June. So, we still need to see any set of numbers that completely reflects the new accounting reality, which I understand to look like »

less tolling revenue & cost of goods sold adjustments,

less overhead cost capitalization through inventory,

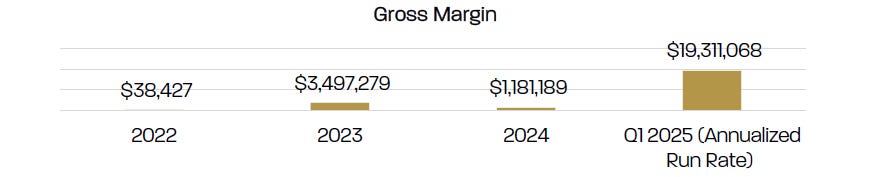

higher gross margins, and

lower inventory intensity

There were clear signs that the first three items are moving in that direction in 2025Q1. The inventory intensity - as I explained in section 2.a. and 2.b. above - is the key question mark in my opinion (imo).

I am encouraged by the 2025Q1 numbers. When companies are exposed to be outright frauds, usually that immediately exposes a balance sheet or funding problem. The 2025/03/31 net debt balance at HASH, however, landed pretty much where I had expected it, and is still tracking to come in around CAD 10m or better by 2025/06/30. Remember, that HASH repaid CAD 3.4m in ANC promissory notes after Q1, through the issuance of shares at a CAD 0.50 share price. In addition, interest payments look manageable with CAD 0.5m in finance costs in 2025Q1 vs over CAD 2m in EBIT. While, the CAD 6m 11% convertible issue only closed 2025/02/13, the additional half a quarter of interest costs won’t make that much difference in 2025Q2. And I did not read anything about new additional financing arrangements.

For the moment, further acquisitions are off the table. That means that the #1 driver of explosive EPS growth is gone for the time-being. On the bright-side, cost savings and earnings contributions from acquisitions integration are still kicking in… and we saw how that improved EBIT (excluding one-offs) from roughly CAD 0.5m in 2024Q4 to over CAD 2m in 2025Q1…

The #1 question was and remains; How will HASH run its working capital management going forward? Profitability is there. But overall free cash flow generation and the economic model will also greatly depend on how management handles inventory, accounts receivable, et cetera. To me, 2025Q1 looked encouraging. The cash burn may as well have been fully explained by the acquisition of cash-strapped acquisitions (Humble in 2025Q1) and the subsequent working capital investments. The next quarter should tell us a bit more. In the back half of 2025, there should be decent visibility.

For convenience, I copied my (earlier paid) remarks on 2025Q1 in footnote 1.

3. Jaminvest resources

Some useful links to key resources on Jaminvest.

🏷️ - Financial models/templates/et cetera (f🔐)

🏷️ - Hong Kong (sub-)portfolio posts

🏷️ - Portfolio posts (f🔐)

» » - Stock/Company list, alphabetical lists of many of the stocks mentioned

🏷️ - Tutorials including Excel sheets

4. Disclaimer

This is neither a recommendation to purchase or sell any of the shares, securities or other instruments mentioned in this document or referred to; nor can this presentation be treated as professional advice to buy, sell or take a position in any shares, securities or other instruments. The information contained herein is based on the study and research of and are merely the written opinions and ideas of the author, and is as such strictly for educational purposes and/or for study or research only. This information should not and cannot be construed as or relied on and (for all intents and purposes) does not constitute financial, investment or any other form of advice. Any investment involves the taking of substantial risks, including (but not limited to) complete loss of capital. Every investor has different strategies, risk tolerances and time frames. You are advised to perform your own independent checks, research or study; and you should contact a licensed professional before making any investment decisions. The author makes it unequivocally clear that there are no warranties, express or implies, as to the accuracy, completeness, or results obtained from any statement, information and/or data set forth herein. The author, shall in no event be held liable to any party for any direct, indirect, punitive, special, incidental, or consequential damages arising directly or indirectly from the use of any of this material.

5. Footnotes

Simply Solventless Concentrates

Chat comments - 2025/06/20

It is still too early (for me) to have a ton of conviction on $HASH.v after the accounting shock with the audited 2024 results, but….

I do find it very encouraging that…

▶️ HASH was already able to sign a distribution agreement, kicking off in July

▶️ The run-rate earnings improved markably from what I calculated after the 2024 results…

…annualized EBIT now already seems to be tracking at CAD 9m, vs my CAD 5m calculation based on the 2024Q4 figures. And remember, growth and incremental cost savings can raise this number further.

▶️ The net debt situation is still tracking in line with the CAD 10m figure I had calculated ‘pro forma’ (which includes the ANC promissory note-for-equity swap)

Of course, the bears raise the argument that HASH has been burning cash… and that was still the case in 2025Q1, as expected and flagged by CEO Swainson.

It will take more time to grow comfort on working capital management from here. From what I see thusfar in Q1 though, the likelihood that the business is hemorrhaging cash has gone down significantly in my opinion.

HASH consolidated a lot of assets with the Humble acquisition, completing late February.

The working capital rate (a) (net working capital / revenue) has almost halved from its peak. Even if management can run the business just with a stable net working capital rate HASH should be able to turn free cash flow positive.

Conclusion: Still too soon to really tell, but Q1 was encouraging to me. Chances of the worst-case (heavy equity dilution or worse) dropped significantly imo.

More is needed from here for a complete share price recovery… but HASH now already seems to be tracking for a valuation of a 4-5x P/E multiple.…before organic growth and incremental cost savings

(a) — Net working capital: (current assets - cash) -/- (current liabilities - debt components)

Do not confuse this traditional net working capital definition with HASH’ working capital measure. The latter is a non-IFRS measure with a very different calculation.