Acomo; A boring hsd % divi yield

This normally boring European healthy foods company seems well on its way to soon provide a growing, high-single-digit dividend yield

1. Intro

In the Founders’ post 🔐 on 👉 2024/07/30, I first brought up two new micro/smallcap ideas. Acomo was one of them. Its 2024Q3 trading update indicates that the company has started to recover from headwinds related to unprecedented volatility in cocoa prices. Two of these indications are

The considerable acceleration in revenue growth from H1 to Q3, driven by a 30% jump in Organic Ingredients segment sales in Q3, “partly due to the higher cocoa prices”.

The management outlook became more positive.

Outlook with 2024H1 results;

Outlook with 2024Q3 trading update;

I do not expect the world from the Acomo stock. What the stock does🤞, is that it adds further diversification to my selection of dividend stocks. The dividend income stream of my portfolio helps cover living expenses, creates financial flexibility and just provides ease-of-mind… yep, sometimes stock investing is just a little bit too exciting… a solid divies income stream adds some tranquility.

Acomo has been around for a looonnnggg time, and likely will continue to be so. I regard it as a business with very low disruption risk. It usually delivers rather boring results, and a steady dividend. Headwinds from the unprecedented volatility in cocoa prices dented results and the stock price, offering (1) a recovery trade on top of (2) the normally attractive dividend, and (3) a bit of growth from the structural demand growth for healthy foods.

I believe after today’s trading update it’s quite likely that Acomo will do EPS of (well) over EUR 1.60 (c11x P/E) and at least an unchanged EUR 1.15 dividend (c6% yield) for 2024...and very likely more in 2025 and beyond. Just returning to the record EUR 1.25 dividend from 2022 offers a 7% yield. As said, I do not expect spectacular investment returns, I just believe that the current EUR 18 share price offers a relatively safe way to lock in annual investment returns that are (significantly) higher than a savings account… just with some added commodity price-related turbulence from time to time.

I copy-pasted the prior Founders’ write-up 🔐 from 2024/07/30 below. I do not think the nature of the company requires a very extensive analysis. If you want to learn more about it, then there are some Seeking Alpha write-ups describing Acomo in more detail. Management has started to improve communications with the investment community. It has already started doing earnings calls, and it has scheduled a Capital Market Day for 2025/04/09.

2. Acomo

Ticker: $ACOMO.as

Market cap: EUR 506m

Original pitch: 2024/07/30

2.a. Description

Acomo is a Rotterdam-based trading firm in spices, nuts, and other food ingredients with some of its own processing facilities. It is not a wide moat business. Yet, it does claim solid market positions: market leader in spices and nuts, global #3 in tea, top 3 in many categories within Tradin Organic and edible seeds. Profit margins are not very high, but given very low capital intensity, Acomo still generates solid free cash flow (FCF) and return on invested capital (ROIC)

2.b. Investment thesis

My attraction to Acomo has been very simple…already since the late ‘90s, early ‘00s.

Dividend; Acomo has been consistently generating solid FCF’s and payout out handsome dividends. Just maintaining the dividend should generate a hsd % dividend return.

A bit of growth; Normally, there should be some growth as Acomo is an enabler to the healthy food trend. Consumers increasingly demand healthy and organic foods. There is a trend towards less sugar, less salt and less fat. That requires spices and natural food ingredients to preserve flavour. In addition, wanting less animal protein leads to more consumption of nuts and seeds.

NB, pricing swings of various commodities and foreign currency can have a substantial impact in any specific time-period.

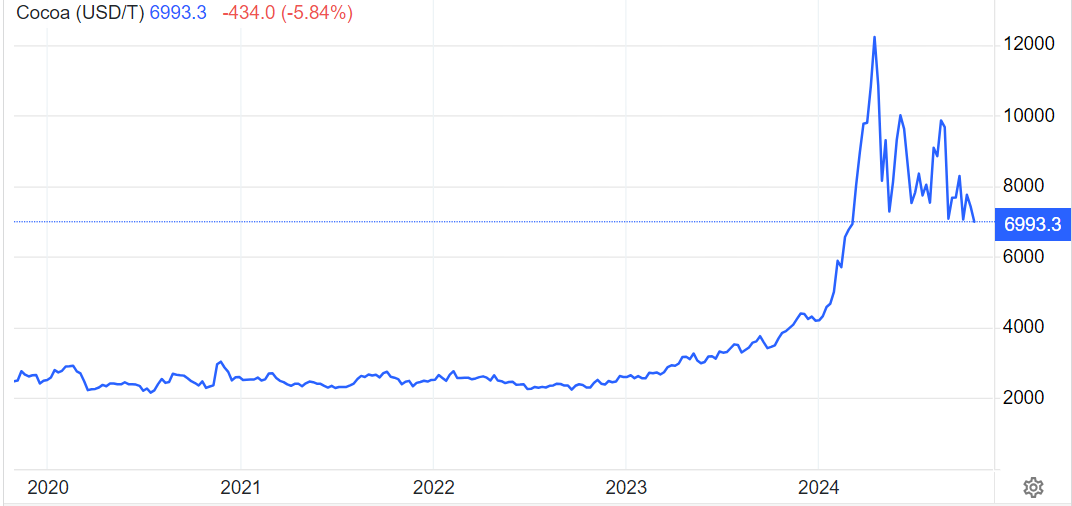

Profit recovery; Profits have been quite stale since the Tradin Organic acquisition, with significant recent pressure on profitability due to hedging-related losses caused by the dramatic volatility in cocoa prices. These losses amounted to about EUR 12m in 2023 and probably another EUR 12m in 2024H1. That is quite significant vs 2022 Adjusted EBITDA of EUR 108m.

Recently, cocao prices have been coming off, and Acomo has been adjusting its hedging execution to shorten time (mismatches). Obviously, ending hedging losses can provide a bit of a boost to earnings. I believe, that profit (margin) boost could help the stock re-rate a bit higher as well.

In addition, Acomo recently announced the acquisition of Caldic’s Nordics nuts & dryfoods business which should add EUR 20m or 1.6% in revenue.

Share price chart

2.c. Catalysts

Investor communication is improving. Management recently started doing webcasts after the halfyearly results announcements. The plan is to host a capital market day after the 2024 results in 2025H1.

2.d. Risks

Commodity price swings; see above

Staff turnover; There has been quite some staff turnover since the large acquisition of Tradin Organic (acquired from SunOpta) at the end of 2020. My assumption is that Acomo returns to its normal boring profitability trackrecord. Elevated staff turnover is a significant risk to such consistent execution.

2.e. Notes

See footnote1.

3. Disclaimer

This is neither a recommendation to purchase or sell any of the shares, securities or other instruments mentioned in this document or referred to; nor can this presentation be treated as professional advice to buy, sell or take a position in any shares, securities or other instruments. The information contained herein is based on the study and research of and are merely the written opinions and ideas of the author, and is as such strictly for educational purposes and/or for study or research only. This information should not and cannot be construed as or relied on and (for all intents and purposes) does not constitute financial, investment or any other form of advice. Any investment involves the taking of substantial risks, including (but not limited to) complete loss of capital. Every investor has different strategies, risk tolerances and time frames. You are advised to perform your own independent checks, research or study; and you should contact a licensed professional before making any investment decisions. The author makes it unequivocally clear that there are no warranties, express or implies, as to the accuracy, completeness, or results obtained from any statement, information and/or data set forth herein. The author, shall in no event be held liable to any party for any direct, indirect, punitive, special, incidental, or consequential damages arising directly or indirectly from the use of any of this material.

4. Footnotes

Acomo

Notes

2024/07/23 2024H1 results

Cocoa prices impacted the Organic ingredients segment

Lower result >100% due to Cocoa

Acquisitions of Caldic’s Nordics nuts & dryfoods business

2024/04/26 AGM

Adjusted EBITDA history, amounts in EUR million

AR 2023

P 58/148 5-year overview

P 58/148 Shareholders as of YE

• Mont Cervin Sarl (12.3%)

• Fidelity Management & Research Company LLC (8.7%)

• Kempen Capital Management N.V. (8.6%)

• Teslin Participaties Coöp UA (8.4%)

• Red Wood Trust (5.0%)

• Lebaras Capital BVBA (5.0%)

P 104/148 Segment disclosures

Geographic disclosures

P 110/148 Bank borrowings

Financial covenants remain unchanged compared to previous year, as follows:

• Interest cover ratio must exceed 4.0x or 3.5x subject to restrictions;

• Solvency must be 30% or higher, or 25% subject to restrictions; and

• Leverage ratio, applicable only on the two portions of the term loan (€103.3 million and $16.7 million), must not exceed 1.6x.

The Company is in full compliance with all covenants.

AR 2022

P 107/144 Bank borrowings

Financial covenants slightly changed compared to previous year, as follows:

• Interest cover ratio must exceed 4.0x or 3.5x in a limited number of cases;

• Solvency must be 30% or higher, or 25% in a limited number of cases; and

• Leverage ratio, applicable only on the two portions of the term loan (€103.3 million and $16.7 million), must not exceed 1.6x.

The Company is in compliance with all covenants, with sufficient headroom.

2021/06/11 Tradin Organic corporate video

2020/11/10 Tradin Organic acquisition

Tradin Organic deal overview. Company was acquired from SunOpta for EUR 330m; EV/S 0.73x, EV/EBITDA 11x.

Acomo businesses by segment