Odd Lots #4; Sintana Energy

A Canadian potential multi-bagger, on massive oil discoveries offshore Namibia.

Introduction

If you have followed the oil & gas industry you’ll probably be familiar with the exploration and development activity in the new and upcoming oil provinces, offshore Guyana and Namibia.

Map #1: Offshore licenses Namibia

Through an investment in one of the oil majors, such as Shell, Total or Chevron, you can build up some exposure. Naturally, that exposure will be quite limited, simply due to the massive overall size of their global operations.

There are other companies that provide much more exposure on the massive potential of these new oil provinces. AlmostMongolian did an extensive write-up on one such company; Africa Oil. Africa Oil $AOI.to / $AOI.st has an effective c3% interest in the Venus oil discovery. Total is the operator of that license and has said that it's at least a 1-2 billion barrels discovery, and it will be developed. Africa Oil is a USD 710m (CAD 958m) market cap company. Just by doing a rough back-of-the-enveloppe calculation, it is not hard to see that only 3% ownership interest can create substantial shareholder value. There is potential for hundreds of millions of USD’s of value, accounting for several tens of percentage points of AOI’s market cap.

Be mindful that the development of these new oil fields will still take many years, and massive sums of capital expenditures. Putting a value on the discoveries is highly speculative at this stage, and unlocking any such value may be years away.

Sintana Energy

Sintana Energy $SEI.v 🏷️ seems to offer the most leverage to offshore Namibia. It is a 100% exploration company. It does not generate any revenue, let alone cash flow from poducing assets. Its fate is (almost) completely tied to the succes or failure to find oil offshore Namibia.

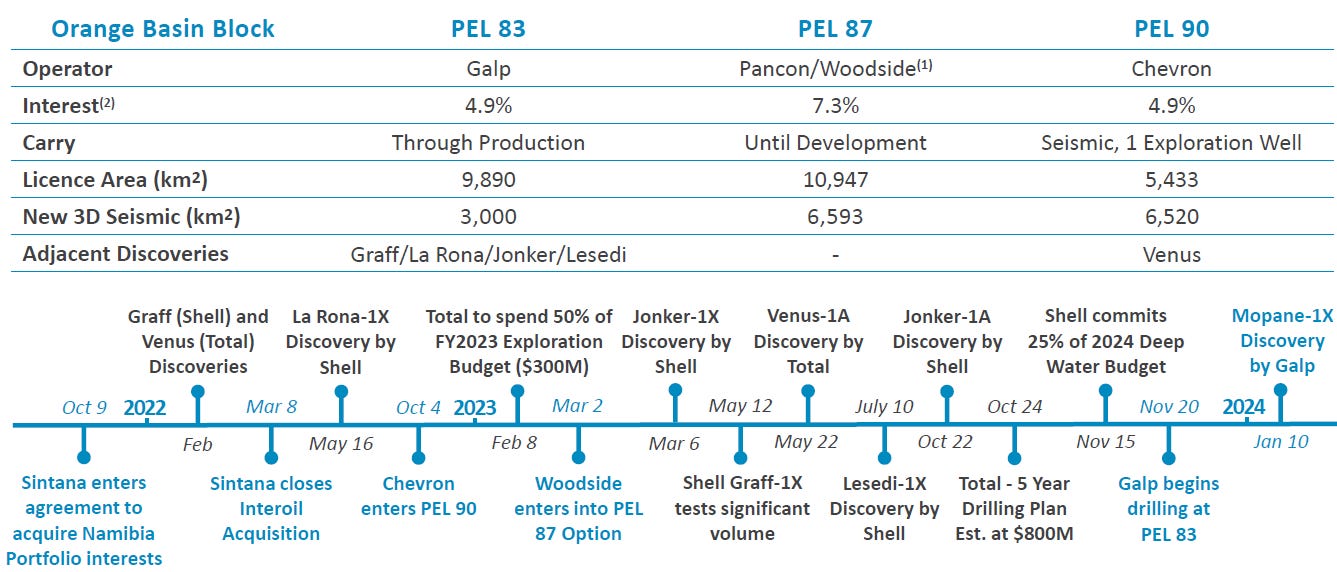

Offshore Namibia license portfolio

As shown on map #1 (above) and map #2 (below), three of Sintana’s offshore licenses (PEL 83 with Galp, PEL90 with Chevron, and PEL87 with Woodside) are in direct vicinity to multi-billion barrel oil finds from Total (in partnership with AOI), Shell, and Galp (Sintana’s partner in block PEL83).

PEL83; Galp Energia the operator on this license announced the third succesful driling operation on 2024/03/14. Drilling operations encountered a significant column of light oil in reservoirs of high quality at the Mopane-2X well. “This third light oil discovery in the Mopane complex and the appraisal results at the AVO-1 reservoir 8 km away from the 1X location provide further evidence of the scale and quality of our exploration portfolio held through our local partners, including Custos” (in which Sintana maintains an indirect 49% interest).

PEL90; Chevron is expected to start drilling at the end of 2024.

PEL87; Woodside could start a drilling campaign in 2025.

Map #2: Offshore licenses Namibia

Looking at the potential valuation outcomes for Sintana (back-of-the-enveloppe calculation below), it is evident that the leverage to Namibian oil discoveries is dramatically bigger than for AOI.

Particularly, when taking into account that Sintana owns 4.9% interests (or better) in three licenses in an area where significant oil discoveries has been made. AOI, on the other hand has only a c3% interest in only one license. AOI is also less risky, though, because it does own cash generating activities in Nigeria.

Other significant advantages for the Sintana thesis include;

Solid balance sheet, particulary after this week’s exercise of 91.6 million warrants, generating approximately $22.5 million in additional cash resources.

Limited capital requirements; Sintana holds carried interests, where the partners are responsible for the exploration (& development) costs. AOI negotiated much worse terms with its partner, Total. While AOI does not have to pay for exploration & development expenses, upfront. These expenses will eventually be settled when oil finally starts to flow.

Margin-of-safety from the three significant oil drilling results already thusfar, by partner Galp Energia. With 394m fully-diluted shares outstanding, every 1bn barrels of recoverable oil should become worth at least (1,000m barrels x $3/b * 5% = USD 150m) or CAD 0.51 per share to Sintana. That is roughly the current share price. I think it is very likely that this value is in place after the three successful drilling results. Moreover, there is still significant further exploration to go not only by Galp, but also by Chevron and Woodside in the other two licenses.

Conclusion; Sintana looks like a potential multi-bagger to me. Every 1bn barrels of recoverable oil should become worth at least CAD 0.51 per share. The company is potentially sitting on multi-billion barrel oil discoveries in not one license, but three. Obviously risks are very high for this stock. Sintana does not have any cash generating assets. If it turns out that development of its licenses is not economical. Then it may be game over for the company. A genuine lottery ticket, but with very favorable odds in my opinion.

Interesting setup here. Could be a multibagger.

I would add that $AOI also has 17% interest on block 3B/4B with a farmout in Orange Basin. It is in South Africas' jurisdiction not Namibias', but still in the same basin than Venus, Sintanas' blocks etc.