Odd lots #15; Open Lending

April Fool's Day is haunting us again; USD 3.15 cash/share takeover offer

Last year on April Fool’s Day, I started posting a series on Open Lending when the stock was being thrown out with the bathwater, while I saw a credible path to make the company great again…

Be greedy when others are Fearful, or...

We will see how this goes, but I think there is an opportunity with investors throwing the baby out with the bathwater… with…

The stock that was available then at USD 1.60-1.70 (and soon afterwards at even lower prices), just received a USD 3.15 cash/share takeover offer from the top customer; AmTrust (via ANV Group Holdings Ltd., which itself was formed through a strategic transaction between AmTrust Financial Services and Blackstone Credit & Insurance).

Not too many people have been interested in this stock. So I won’t waste too much time on it, but… I will give a couple of updated thoughts…

Jaminvest resources

Some useful links to key resources on Jaminvest.

🏷️ - Financial models/templates/et cetera (f🔐)

🏷️ - Hong Kong (sub-)portfolio posts

🏷️ - Portfolio posts (f🔐)

» » - Stock/Company list (2026), alphabetical lists of many of the stocks mentioned

🏷️ - Tutorials including Excel sheets

Please find the disclaimer for all @Jam_invest content » here.

1. My takeaways 🏷️

I feel that last year’s April Fool’s Day is haunting (minority) shareholders in Open Lending LPRO.us once again. Last year this baby (= LPRO stock) was thrown out with the bathwater. This year should’ve been the year that the company would demonstrate a return to revenue growth, but… instead of reaping the benefits of revenue growth on a rationalized and predominantly fixed-base expense base, the Board is trying to sell the company at (what looks to be) the bottom of the cycle. Normally, in such a situation (minority) shareholders should revolt, try to stop the takeover, shop for another offer, et cetera. In this situation, however, that is complicated because the acquirer is the top client, AmTrust (through ANV Group Holdings). An alternative offer would most likely thwart the top client, and risk losing its business… (likely) considerably impairing LPRO’s economics (because I am not sure that the other insurance partners would fill up a big void left by AmTrust). Therefore, personally, I don’t see an alternative acquisition as very likely… and I think the best that the bulls on LPRO can hope for, longer-term, is that the offer is not accepted by (the majority of) shareholders… retaining the long-term upside potential on the stock if/when LPRO indeed delivers on a return to revenue growth (with very little incremental expense growth)… and naturally also retaining the execution risk and the risk towards the external environment (remember that LPRO is heavily reliant on overall car sales in the U.S.).

I have obviously no clue whether this takeover is going to conclude or not. On the one hand I think there are a lot of pretty much un-interested shareholders for who LPRO only comprises a tiny portion of their portfolio... that they can now exit with a short-term premium. On the other hand, the acquisition offer substantially undervalues the “return to growth” scenario for LPRO and it does not look like that much of the share-ownership has been committed to the offer (after a quick scan of the documents, I arrive at roughly 16% ownership). If I had to guess, the scenarios of a) the takeover succeeding at USD 3.15, and b) the takeover failing in part or completely and LPRO remaining a listed company, seem most likely to me. With that, I don’t see meaningful upside in the stock, here at USD 3.11, in the very short-term… and I have therefore exited.

2. Merger agreement

I put some titbits of the merger agreement and the press release in footnote 1. Highlights include…

“The transaction has been unanimously approved by the Open Lending Board of Directors and is expected to close in the third quarter of 2026, subject to customary closing conditions, including the receipt of regulatory approvals and the tender of shares of Open Lending common stock representing a majority of the outstanding shares of Open Lending common stock.”

The termination fee is USD 13.6m, payable by (“the Company”) Open Lending upon ao’s the acceptance of a superior offer

3. Footnotes

Merger agreement - titbits

Glossary

the Company = Open Lending

the Parent = ANV Group Holdings Ltd

…

Takeover offer USD 3.15 cash per share

The transaction has been unanimously approved by the Open Lending Board of Directors and is expected to close in the third quarter of 2026, subject to customary closing conditions, including the receipt of regulatory approvals and the tender of shares of Open Lending common stock representing a majority of the outstanding shares of Open Lending common stock.

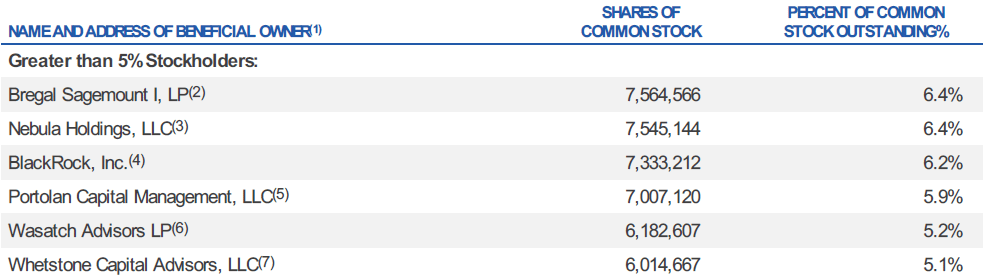

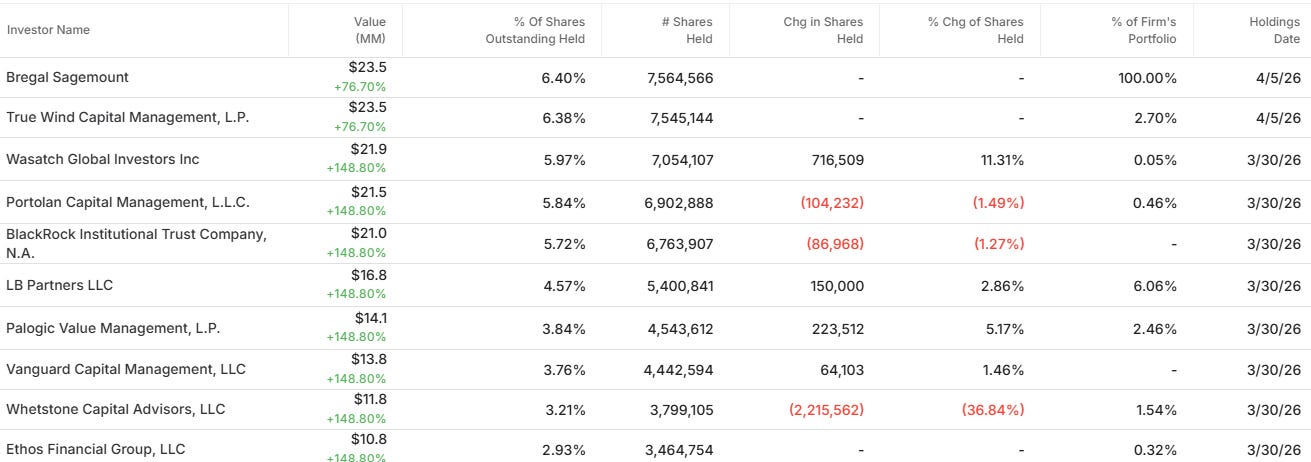

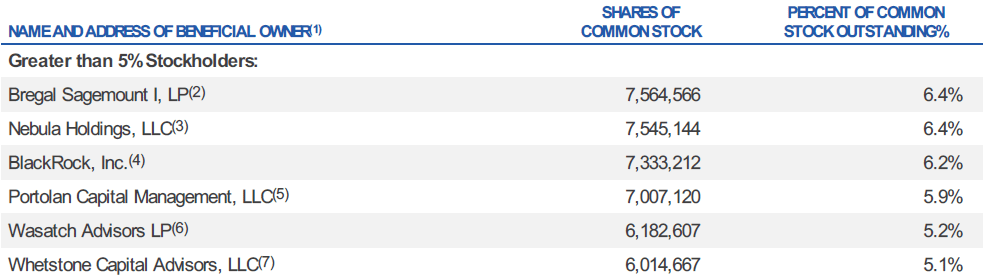

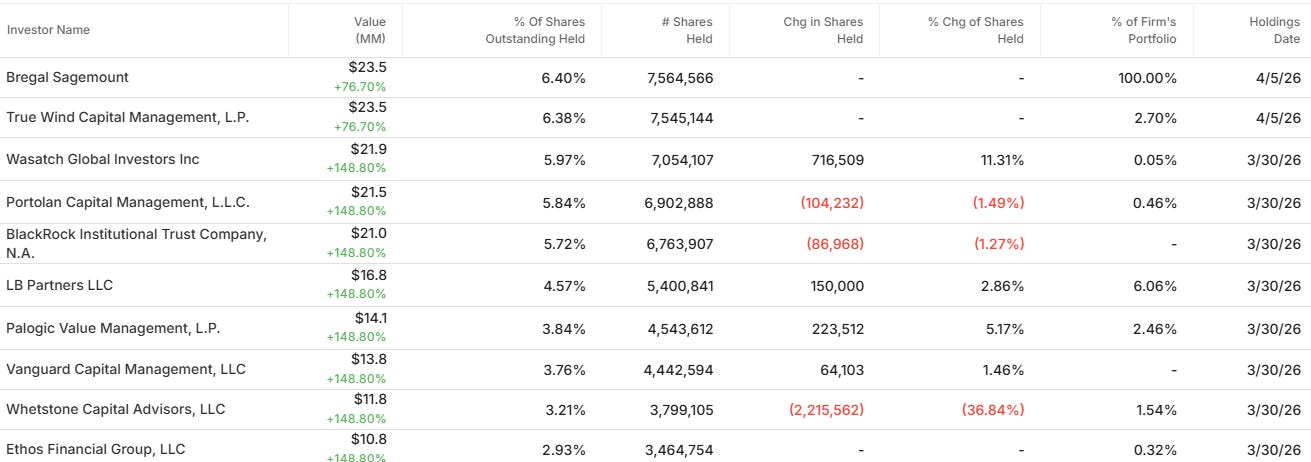

The private equity funds Bregal Sagemount I, L.P. and Nebula Holdings, LLC (and its “managing member” True Wind Capital, L.P.) have committed their shares for the offer….

Moreover, the Board unanimously votes in favor of the takeover offer… So, I suppose that Palogic Value, represented on the Board by William Dabbs Cavin, will submit its shares to the offer as well.

That implies that c16% of the outstanding shares are committed to the offer… leaving a lot of potential for the acquisition to fail, ie fewer than the majority of shares are submitted to the offer.

Top shareholders, as of 2026/04/06…

Top shareholders, according to Tikr…

The Merger Agreement contains certain termination rights for the Company and Parent. Either party may terminate the Merger Agreement if the Offer has not been consummated by 11:59 p.m. Eastern Time on October 15, 2026, which date will be automatically extended to December 15, 2026 if all of the conditions to the Offer have been satisfied or waived except for the Regulatory Condition or certain related legal restraints (the “Outside Date”)

The Company has agreed to pay Parent a termination fee of $13,580,000 in cash upon termination of the Merger Agreement under certain specified circumstances, including (i) termination by the Company to enter into a Superior Proposal, (ii) termination by Parent following an adverse recommendation change by the Company Board, or (iii) termination under certain other circumstances (including for failure to consummate by

the Outside Date, satisfy the Minimum Condition, or Company breach) where an Acquisition Proposal (as defined in the Merger Agreement) has been publicly announced and a definitive agreement is subsequently entered into within twelve months.

Great call Jam!